0001601712false2022Q3December 31http://fasb.org/us-gaap/2022#OtherAssetshttp://fasb.org/us-gaap/2022#OtherAssets00016017122022-01-012022-09-300001601712us-gaap:CommonStockMember2022-01-012022-09-300001601712us-gaap:SeriesAPreferredStockMember2022-01-012022-09-3000016017122022-10-21xbrli:shares00016017122022-07-012022-09-30iso4217:USD00016017122021-07-012021-09-3000016017122021-01-012021-09-300001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-07-012022-09-300001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-07-012021-09-300001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-01-012022-09-300001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-01-012021-09-30iso4217:USDxbrli:shares00016017122022-09-3000016017122021-12-310001601712syf:UnsecuritizedLoansHeldforInvestmentMember2022-09-300001601712syf:UnsecuritizedLoansHeldforInvestmentMember2021-12-310001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-09-300001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-12-310001601712us-gaap:PreferredStockMember2020-12-310001601712us-gaap:CommonStockMember2020-12-310001601712us-gaap:AdditionalPaidInCapitalMember2020-12-310001601712us-gaap:RetainedEarningsMember2020-12-310001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001601712us-gaap:TreasuryStockCommonMember2020-12-3100016017122020-12-310001601712us-gaap:RetainedEarningsMember2021-01-012021-03-3100016017122021-01-012021-03-310001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-03-310001601712us-gaap:TreasuryStockCommonMember2021-01-012021-03-310001601712us-gaap:CommonStockMember2021-01-012021-03-310001601712us-gaap:AdditionalPaidInCapitalMember2021-01-012021-03-310001601712us-gaap:PreferredStockMember2021-03-310001601712us-gaap:CommonStockMember2021-03-310001601712us-gaap:AdditionalPaidInCapitalMember2021-03-310001601712us-gaap:RetainedEarningsMember2021-03-310001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-03-310001601712us-gaap:TreasuryStockCommonMember2021-03-3100016017122021-03-310001601712us-gaap:RetainedEarningsMember2021-04-012021-06-3000016017122021-04-012021-06-300001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-04-012021-06-300001601712us-gaap:TreasuryStockCommonMember2021-04-012021-06-300001601712us-gaap:CommonStockMember2021-04-012021-06-300001601712us-gaap:AdditionalPaidInCapitalMember2021-04-012021-06-300001601712us-gaap:PreferredStockMember2021-06-300001601712us-gaap:CommonStockMember2021-06-300001601712us-gaap:AdditionalPaidInCapitalMember2021-06-300001601712us-gaap:RetainedEarningsMember2021-06-300001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-06-300001601712us-gaap:TreasuryStockCommonMember2021-06-3000016017122021-06-300001601712us-gaap:RetainedEarningsMember2021-07-012021-09-300001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-07-012021-09-300001601712us-gaap:TreasuryStockCommonMember2021-07-012021-09-300001601712us-gaap:CommonStockMember2021-07-012021-09-300001601712us-gaap:AdditionalPaidInCapitalMember2021-07-012021-09-300001601712us-gaap:PreferredStockMember2021-09-300001601712us-gaap:CommonStockMember2021-09-300001601712us-gaap:AdditionalPaidInCapitalMember2021-09-300001601712us-gaap:RetainedEarningsMember2021-09-300001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-09-300001601712us-gaap:TreasuryStockCommonMember2021-09-3000016017122021-09-300001601712us-gaap:PreferredStockMember2021-12-310001601712us-gaap:CommonStockMember2021-12-310001601712us-gaap:AdditionalPaidInCapitalMember2021-12-310001601712us-gaap:RetainedEarningsMember2021-12-310001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001601712us-gaap:TreasuryStockCommonMember2021-12-310001601712us-gaap:RetainedEarningsMember2022-01-012022-03-3100016017122022-01-012022-03-310001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-03-310001601712us-gaap:TreasuryStockCommonMember2022-01-012022-03-310001601712us-gaap:CommonStockMember2022-01-012022-03-310001601712us-gaap:AdditionalPaidInCapitalMember2022-01-012022-03-310001601712us-gaap:PreferredStockMember2022-03-310001601712us-gaap:CommonStockMember2022-03-310001601712us-gaap:AdditionalPaidInCapitalMember2022-03-310001601712us-gaap:RetainedEarningsMember2022-03-310001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-03-310001601712us-gaap:TreasuryStockCommonMember2022-03-3100016017122022-03-310001601712us-gaap:RetainedEarningsMember2022-04-012022-06-3000016017122022-04-012022-06-300001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-04-012022-06-300001601712us-gaap:TreasuryStockCommonMember2022-04-012022-06-300001601712us-gaap:CommonStockMember2022-04-012022-06-300001601712us-gaap:AdditionalPaidInCapitalMember2022-04-012022-06-300001601712us-gaap:PreferredStockMember2022-06-300001601712us-gaap:CommonStockMember2022-06-300001601712us-gaap:AdditionalPaidInCapitalMember2022-06-300001601712us-gaap:RetainedEarningsMember2022-06-300001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-06-300001601712us-gaap:TreasuryStockCommonMember2022-06-3000016017122022-06-300001601712us-gaap:RetainedEarningsMember2022-07-012022-09-300001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-07-012022-09-300001601712us-gaap:TreasuryStockCommonMember2022-07-012022-09-300001601712us-gaap:CommonStockMember2022-07-012022-09-300001601712us-gaap:AdditionalPaidInCapitalMember2022-07-012022-09-300001601712us-gaap:PreferredStockMember2022-09-300001601712us-gaap:CommonStockMember2022-09-300001601712us-gaap:AdditionalPaidInCapitalMember2022-09-300001601712us-gaap:RetainedEarningsMember2022-09-300001601712us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-09-300001601712us-gaap:TreasuryStockCommonMember2022-09-300001601712us-gaap:USGovernmentCorporationsAndAgenciesSecuritiesMember2022-09-300001601712us-gaap:USGovernmentCorporationsAndAgenciesSecuritiesMember2021-12-310001601712us-gaap:USStatesAndPoliticalSubdivisionsMember2022-09-300001601712us-gaap:USStatesAndPoliticalSubdivisionsMember2021-12-310001601712us-gaap:ResidentialMortgageBackedSecuritiesMember2022-09-300001601712us-gaap:ResidentialMortgageBackedSecuritiesMember2021-12-310001601712us-gaap:AssetBackedSecuritiesMember2022-09-300001601712us-gaap:AssetBackedSecuritiesMember2021-12-310001601712us-gaap:OtherDebtSecuritiesMember2022-09-300001601712us-gaap:OtherDebtSecuritiesMember2021-12-31xbrli:pure00016017122022-01-012022-06-300001601712us-gaap:CreditCardReceivablesMember2022-09-300001601712us-gaap:CreditCardReceivablesMember2021-12-310001601712us-gaap:ConsumerLoanMember2022-09-300001601712us-gaap:ConsumerLoanMember2021-12-310001601712us-gaap:CommercialPortfolioSegmentMember2022-09-300001601712us-gaap:CommercialPortfolioSegmentMember2021-12-310001601712us-gaap:UnallocatedFinancingReceivablesMember2022-09-300001601712us-gaap:UnallocatedFinancingReceivablesMember2021-12-310001601712us-gaap:CreditCardReceivablesMember2022-06-300001601712us-gaap:CreditCardReceivablesMember2022-07-012022-09-300001601712us-gaap:ConsumerLoanMember2022-06-300001601712us-gaap:ConsumerLoanMember2022-07-012022-09-300001601712us-gaap:CommercialPortfolioSegmentMember2022-06-300001601712us-gaap:CommercialPortfolioSegmentMember2022-07-012022-09-300001601712us-gaap:UnallocatedFinancingReceivablesMember2022-06-300001601712us-gaap:UnallocatedFinancingReceivablesMember2022-07-012022-09-300001601712us-gaap:CreditCardReceivablesMember2021-06-300001601712us-gaap:CreditCardReceivablesMember2021-07-012021-09-300001601712us-gaap:CreditCardReceivablesMember2021-09-300001601712us-gaap:ConsumerLoanMember2021-06-300001601712us-gaap:ConsumerLoanMember2021-07-012021-09-300001601712us-gaap:ConsumerLoanMember2021-09-300001601712us-gaap:CommercialPortfolioSegmentMember2021-06-300001601712us-gaap:CommercialPortfolioSegmentMember2021-07-012021-09-300001601712us-gaap:CommercialPortfolioSegmentMember2021-09-300001601712us-gaap:UnallocatedFinancingReceivablesMember2021-06-300001601712us-gaap:UnallocatedFinancingReceivablesMember2021-07-012021-09-300001601712us-gaap:UnallocatedFinancingReceivablesMember2021-09-300001601712us-gaap:CreditCardReceivablesMember2022-01-012022-09-300001601712us-gaap:ConsumerLoanMember2022-01-012022-09-300001601712us-gaap:CommercialPortfolioSegmentMember2022-01-012022-09-300001601712us-gaap:UnallocatedFinancingReceivablesMember2022-01-012022-09-300001601712us-gaap:CreditCardReceivablesMember2020-12-310001601712us-gaap:CreditCardReceivablesMember2021-01-012021-09-300001601712us-gaap:ConsumerLoanMember2020-12-310001601712us-gaap:ConsumerLoanMember2021-01-012021-09-300001601712us-gaap:CommercialPortfolioSegmentMember2020-12-310001601712us-gaap:CommercialPortfolioSegmentMember2021-01-012021-09-300001601712us-gaap:UnallocatedFinancingReceivablesMember2020-12-310001601712us-gaap:UnallocatedFinancingReceivablesMember2021-01-012021-09-300001601712syf:FinancingReceivables30to89DaysPastDueMemberus-gaap:CreditCardReceivablesMember2022-09-300001601712us-gaap:CreditCardReceivablesMemberus-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMember2022-09-300001601712us-gaap:FinancialAssetPastDueMemberus-gaap:CreditCardReceivablesMember2022-09-300001601712syf:FinancingReceivables30to89DaysPastDueMemberus-gaap:ConsumerLoanMember2022-09-300001601712us-gaap:ConsumerLoanMemberus-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMember2022-09-300001601712us-gaap:FinancialAssetPastDueMemberus-gaap:ConsumerLoanMember2022-09-300001601712syf:FinancingReceivables30to89DaysPastDueMemberus-gaap:CommercialPortfolioSegmentMember2022-09-300001601712us-gaap:CommercialPortfolioSegmentMemberus-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMember2022-09-300001601712us-gaap:FinancialAssetPastDueMemberus-gaap:CommercialPortfolioSegmentMember2022-09-300001601712syf:FinancingReceivables30to89DaysPastDueMember2022-09-300001601712us-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMember2022-09-300001601712us-gaap:FinancialAssetPastDueMember2022-09-300001601712syf:FinancingReceivables30to89DaysPastDueMemberus-gaap:CreditCardReceivablesMember2021-12-310001601712us-gaap:CreditCardReceivablesMemberus-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMember2021-12-310001601712us-gaap:FinancialAssetPastDueMemberus-gaap:CreditCardReceivablesMember2021-12-310001601712syf:FinancingReceivables30to89DaysPastDueMemberus-gaap:ConsumerLoanMember2021-12-310001601712us-gaap:ConsumerLoanMemberus-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMember2021-12-310001601712us-gaap:FinancialAssetPastDueMemberus-gaap:ConsumerLoanMember2021-12-310001601712syf:FinancingReceivables30to89DaysPastDueMemberus-gaap:CommercialPortfolioSegmentMember2021-12-310001601712us-gaap:CommercialPortfolioSegmentMemberus-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMember2021-12-310001601712us-gaap:FinancialAssetPastDueMemberus-gaap:CommercialPortfolioSegmentMember2021-12-310001601712syf:FinancingReceivables30to89DaysPastDueMember2021-12-310001601712us-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMember2021-12-310001601712us-gaap:FinancialAssetPastDueMember2021-12-31syf:contract0001601712syf:SixHundredAndFiftyOneOrHigherMemberus-gaap:CreditCardReceivablesMember2022-09-300001601712syf:FiveHundredAndNinetyOneToSixHundredAndFiftyMemberus-gaap:CreditCardReceivablesMember2022-09-300001601712syf:FiveHundredAndNinetyOrLessMemberus-gaap:CreditCardReceivablesMember2022-09-300001601712syf:SixHundredAndFiftyOneOrHigherMemberus-gaap:CreditCardReceivablesMember2021-12-310001601712syf:FiveHundredAndNinetyOneToSixHundredAndFiftyMemberus-gaap:CreditCardReceivablesMember2021-12-310001601712syf:FiveHundredAndNinetyOrLessMemberus-gaap:CreditCardReceivablesMember2021-12-310001601712syf:SixHundredAndFiftyOneOrHigherMemberus-gaap:CreditCardReceivablesMember2021-09-300001601712syf:FiveHundredAndNinetyOneToSixHundredAndFiftyMemberus-gaap:CreditCardReceivablesMember2021-09-300001601712syf:FiveHundredAndNinetyOrLessMemberus-gaap:CreditCardReceivablesMember2021-09-300001601712syf:SixHundredAndFiftyOneOrHigherMemberus-gaap:ConsumerLoanMember2022-09-300001601712syf:FiveHundredAndNinetyOneToSixHundredAndFiftyMemberus-gaap:ConsumerLoanMember2022-09-300001601712syf:FiveHundredAndNinetyOrLessMemberus-gaap:ConsumerLoanMember2022-09-300001601712syf:SixHundredAndFiftyOneOrHigherMemberus-gaap:ConsumerLoanMember2021-12-310001601712syf:FiveHundredAndNinetyOneToSixHundredAndFiftyMemberus-gaap:ConsumerLoanMember2021-12-310001601712syf:FiveHundredAndNinetyOrLessMemberus-gaap:ConsumerLoanMember2021-12-310001601712syf:SixHundredAndFiftyOneOrHigherMemberus-gaap:ConsumerLoanMember2021-09-300001601712syf:FiveHundredAndNinetyOneToSixHundredAndFiftyMemberus-gaap:ConsumerLoanMember2021-09-300001601712syf:FiveHundredAndNinetyOrLessMemberus-gaap:ConsumerLoanMember2021-09-300001601712syf:SixHundredAndFiftyOneOrHigherMemberus-gaap:CommercialPortfolioSegmentMember2022-09-300001601712us-gaap:CommercialPortfolioSegmentMembersyf:FiveHundredAndNinetyOneToSixHundredAndFiftyMember2022-09-300001601712syf:FiveHundredAndNinetyOrLessMemberus-gaap:CommercialPortfolioSegmentMember2022-09-300001601712syf:SixHundredAndFiftyOneOrHigherMemberus-gaap:CommercialPortfolioSegmentMember2021-12-310001601712us-gaap:CommercialPortfolioSegmentMembersyf:FiveHundredAndNinetyOneToSixHundredAndFiftyMember2021-12-310001601712syf:FiveHundredAndNinetyOrLessMemberus-gaap:CommercialPortfolioSegmentMember2021-12-310001601712syf:SixHundredAndFiftyOneOrHigherMemberus-gaap:CommercialPortfolioSegmentMember2021-09-300001601712us-gaap:CommercialPortfolioSegmentMembersyf:FiveHundredAndNinetyOneToSixHundredAndFiftyMember2021-09-300001601712syf:FiveHundredAndNinetyOrLessMemberus-gaap:CommercialPortfolioSegmentMember2021-09-300001601712syf:InvestmentsFundingCommitmentMember2022-09-300001601712us-gaap:CustomerRelatedIntangibleAssetsMember2022-09-300001601712us-gaap:CustomerRelatedIntangibleAssetsMember2021-12-310001601712us-gaap:ComputerSoftwareIntangibleAssetMember2022-09-300001601712us-gaap:ComputerSoftwareIntangibleAssetMember2021-12-310001601712us-gaap:CustomerRelatedIntangibleAssetsMember2022-01-012022-09-300001601712us-gaap:CustomerRelatedIntangibleAssetsMember2021-01-012021-09-300001601712us-gaap:CustomerContractsMemberus-gaap:SellingAndMarketingExpenseMember2022-07-012022-09-300001601712us-gaap:CustomerContractsMemberus-gaap:SellingAndMarketingExpenseMember2021-07-012021-09-300001601712us-gaap:CustomerContractsMemberus-gaap:SellingAndMarketingExpenseMember2022-01-012022-09-300001601712us-gaap:CustomerContractsMemberus-gaap:SellingAndMarketingExpenseMember2021-01-012021-09-300001601712syf:FiniteLivedIntangibleAssetsExcludingCustomerContractsMemberus-gaap:OtherExpenseMember2022-07-012022-09-300001601712syf:FiniteLivedIntangibleAssetsExcludingCustomerContractsMemberus-gaap:OtherExpenseMember2021-07-012021-09-300001601712syf:FiniteLivedIntangibleAssetsExcludingCustomerContractsMemberus-gaap:OtherExpenseMember2022-01-012022-09-300001601712syf:FiniteLivedIntangibleAssetsExcludingCustomerContractsMemberus-gaap:OtherExpenseMember2021-01-012021-09-300001601712syf:ProgramArrangerMember2022-09-300001601712syf:FixedSecuritizedBorrowingsMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMembersrt:MinimumMember2022-09-300001601712syf:FixedSecuritizedBorrowingsMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMembersrt:MaximumMember2022-09-300001601712syf:FixedSecuritizedBorrowingsMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-09-300001601712syf:FixedSecuritizedBorrowingsMemberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-12-310001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMembersyf:FloatingSecuritizedBorrowingsMembersrt:MinimumMember2022-09-300001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMembersrt:MaximumMembersyf:FloatingSecuritizedBorrowingsMember2022-09-300001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMembersyf:FloatingSecuritizedBorrowingsMember2022-09-300001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMembersyf:FloatingSecuritizedBorrowingsMember2021-12-310001601712srt:MinimumMemberus-gaap:SeniorNotesMembersyf:FixedSeniorUnsecuredNotesMember2022-09-300001601712srt:MaximumMemberus-gaap:SeniorNotesMembersyf:FixedSeniorUnsecuredNotesMember2022-09-300001601712us-gaap:SeniorNotesMembersyf:FixedSeniorUnsecuredNotesMember2022-09-300001601712us-gaap:SeniorNotesMembersyf:FixedSeniorUnsecuredNotesMember2021-12-310001601712srt:MinimumMemberus-gaap:SeniorNotesMembersrt:SubsidiariesMembersyf:FixedSeniorUnsecuredNotesMember2022-09-300001601712srt:MaximumMemberus-gaap:SeniorNotesMembersrt:SubsidiariesMembersyf:FixedSeniorUnsecuredNotesMember2022-09-300001601712us-gaap:SeniorNotesMembersrt:SubsidiariesMembersyf:FixedSeniorUnsecuredNotesMember2022-09-300001601712us-gaap:SeniorNotesMembersrt:SubsidiariesMembersyf:FixedSeniorUnsecuredNotesMember2021-12-310001601712us-gaap:SeniorNotesMember2022-09-300001601712us-gaap:SeniorNotesMember2021-12-310001601712us-gaap:SeniorNotesMembersyf:FixedRateSeniorNotesDue2025Member2022-09-300001601712us-gaap:SeniorNotesMembersrt:SubsidiariesMembersyf:FixedRateSeniorNotesDue2025Member2022-09-300001601712syf:FixedRateSeniorNotesDue2027Memberus-gaap:SeniorNotesMembersrt:SubsidiariesMember2022-09-300001601712us-gaap:UnsecuredDebtMemberus-gaap:RevolvingCreditFacilityMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentCorporationsAndAgenciesSecuritiesMemberus-gaap:FairValueInputsLevel1Member2022-09-300001601712us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentCorporationsAndAgenciesSecuritiesMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberus-gaap:USGovernmentCorporationsAndAgenciesSecuritiesMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentCorporationsAndAgenciesSecuritiesMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueInputsLevel1Member2022-09-300001601712us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USStatesAndPoliticalSubdivisionsMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueInputsLevel3Member2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USStatesAndPoliticalSubdivisionsMember2022-09-300001601712us-gaap:ResidentialMortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2022-09-300001601712us-gaap:FairValueInputsLevel2Memberus-gaap:ResidentialMortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2022-09-300001601712us-gaap:ResidentialMortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2022-09-300001601712us-gaap:ResidentialMortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberus-gaap:AssetBackedSecuritiesMember2022-09-300001601712us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:AssetBackedSecuritiesMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberus-gaap:AssetBackedSecuritiesMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:AssetBackedSecuritiesMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:OtherDebtSecuritiesMemberus-gaap:FairValueInputsLevel1Member2022-09-300001601712us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:OtherDebtSecuritiesMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:OtherDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:OtherDebtSecuritiesMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2022-09-300001601712us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMember2022-09-300001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentCorporationsAndAgenciesSecuritiesMemberus-gaap:FairValueInputsLevel1Member2021-12-310001601712us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentCorporationsAndAgenciesSecuritiesMember2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberus-gaap:USGovernmentCorporationsAndAgenciesSecuritiesMember2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USGovernmentCorporationsAndAgenciesSecuritiesMember2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueInputsLevel1Member2021-12-310001601712us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USStatesAndPoliticalSubdivisionsMember2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueInputsLevel3Member2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USStatesAndPoliticalSubdivisionsMember2021-12-310001601712us-gaap:ResidentialMortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2021-12-310001601712us-gaap:FairValueInputsLevel2Memberus-gaap:ResidentialMortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001601712us-gaap:ResidentialMortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2021-12-310001601712us-gaap:ResidentialMortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberus-gaap:AssetBackedSecuritiesMember2021-12-310001601712us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:AssetBackedSecuritiesMember2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberus-gaap:AssetBackedSecuritiesMember2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:AssetBackedSecuritiesMember2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:OtherDebtSecuritiesMemberus-gaap:FairValueInputsLevel1Member2021-12-310001601712us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:OtherDebtSecuritiesMember2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:OtherDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:OtherDebtSecuritiesMember2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2021-12-310001601712us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2021-12-310001601712us-gaap:FairValueMeasurementsRecurringMember2021-12-310001601712us-gaap:CarryingReportedAmountFairValueDisclosureMember2022-09-300001601712us-gaap:FairValueInputsLevel1Member2022-09-300001601712us-gaap:FairValueInputsLevel2Member2022-09-300001601712us-gaap:FairValueInputsLevel3Member2022-09-300001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2022-09-300001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMemberus-gaap:FairValueInputsLevel1Member2022-09-300001601712us-gaap:FairValueInputsLevel2Memberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-09-300001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMemberus-gaap:FairValueInputsLevel3Member2022-09-300001601712us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:SeniorNotesMember2022-09-300001601712us-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel1Member2022-09-300001601712us-gaap:FairValueInputsLevel2Memberus-gaap:SeniorNotesMember2022-09-300001601712us-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel3Member2022-09-300001601712us-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310001601712us-gaap:FairValueInputsLevel1Member2021-12-310001601712us-gaap:FairValueInputsLevel2Member2021-12-310001601712us-gaap:FairValueInputsLevel3Member2021-12-310001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMemberus-gaap:FairValueInputsLevel1Member2021-12-310001601712us-gaap:FairValueInputsLevel2Memberus-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-12-310001601712us-gaap:VariableInterestEntityPrimaryBeneficiaryMemberus-gaap:FairValueInputsLevel3Member2021-12-310001601712us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:SeniorNotesMember2021-12-310001601712us-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel1Member2021-12-310001601712us-gaap:FairValueInputsLevel2Memberus-gaap:SeniorNotesMember2021-12-310001601712us-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel3Member2021-12-310001601712syf:BaselIIIMember2022-09-300001601712syf:BaselIIIMember2021-12-310001601712srt:SubsidiariesMembersyf:BaselIIIMember2022-09-300001601712srt:SubsidiariesMembersyf:BaselIIIMember2021-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| | | | | |

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2022

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

001-36560

(Commission File Number)

SYNCHRONY FINANCIAL

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 51-0483352 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer

Identification No.) |

| | | | | | | | | | | |

| 777 Long Ridge Road | | |

| Stamford, | Connecticut | | 06902 |

| (Address of principal executive offices) | | (Zip Code) |

(Registrant’s telephone number, including area code) - (203) 585-2400

Securities Registered Pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common stock, par value $0.001 per share | SYF | New York Stock Exchange |

| Depositary Shares Each Representing a 1/40th Interest in a Share of 5.625% Fixed Rate Non-Cumulative Perpetual Preferred Stock, Series A | SYFPrA | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large Accelerated Filer | ☒ | Accelerated Filer | ☐ |

| | | |

| Non-Accelerated Filer | ☐ | Smaller Reporting Company | ☐ |

| | | |

| | Emerging Growth Company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The number of shares of the registrant’s common stock, par value $0.001 per share, outstanding as of October 21, 2022 was 450,541,428.

Synchrony Financial

| | | | | |

| PART I - FINANCIAL INFORMATION | Page |

| |

| |

| Item 1. Financial Statements: | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| PART II - OTHER INFORMATION | |

| |

| |

| |

| |

| |

| |

Item 6. Exhibits | |

| |

Certain Defined Terms

Except as the context may otherwise require in this report, references to:

•“we,” “us,” “our” and the “Company” are to SYNCHRONY FINANCIAL and its subsidiaries;

•“Synchrony” are to SYNCHRONY FINANCIAL only;

•the “Bank” are to Synchrony Bank (a subsidiary of Synchrony);

•the “Board of Directors” or “Board” are to Synchrony's board of directors;

•“CECL” are to the impairment model known as the Current Expected Credit Loss model, which is based on expected credit losses; and

•“VantageScore” are to a credit score developed by the three major credit reporting agencies which is used as a means of evaluating the likelihood that credit users will pay their obligations.

We provide a range of credit products through programs we have established with a diverse group of national and regional retailers, local merchants, manufacturers, buying groups, industry associations and healthcare service providers, which, in our business and in this report, we refer to as our “partners.” The terms of the programs all require cooperative efforts between us and our partners of varying natures and degrees to establish and operate the programs. Our use of the term “partners” to refer to these entities is not intended to, and does not, describe our legal relationship with them, imply that a legal partnership or other relationship exists between the parties or create any legal partnership or other relationship.

Unless otherwise indicated, references to “loan receivables” do not include loan receivables held for sale.

For a description of certain other terms we use, including “active account” and “purchase volume,” see the notes to “Management’s Discussion and Analysis—Results of Operations—Other Financial and Statistical Data” in our Annual Report on Form 10-K for the year ended December 31, 2021 (our “2021 Form 10-K”). There is no standard industry definition for many of these terms, and other companies may define them differently than we do.

“Synchrony” and its logos and other trademarks referred to in this report, including CareCredit®, Quickscreen®, Dual Card™, Synchrony Car Care™ and SyPI™, belong to us. Solely for convenience, we refer to our trademarks in this report without the ™ and ® symbols, but such references are not intended to indicate that we will not assert, to the fullest extent under applicable law, our rights to our trademarks. Other service marks, trademarks and trade names referred to in this report are the property of their respective owners.

On our website at www.synchrony.com, we make available under the "Investors-SEC Filings" menu selection, free of charge, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after such reports or amendments are electronically filed with, or furnished to, the SEC. The SEC maintains an Internet site at www.sec.gov that contains reports, proxy and information statements, and other information that we file electronically with the SEC.

Cautionary Note Regarding Forward-Looking Statements:

Various statements in this Quarterly Report on Form 10-Q may contain “forward-looking statements” as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which are subject to the “safe harbor” created by those sections. Forward-looking statements may be identified by words such as “expects,” “intends,” “anticipates,” “plans,” “believes,” “seeks,” “targets,” “outlook,” “estimates,” “will,” “should,” “may” or words of similar meaning, but these words are not the exclusive means of identifying forward-looking statements.

Forward-looking statements are based on management’s current expectations and assumptions, and are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. As a result, actual results could differ materially from those indicated in these forward-looking statements. Factors that could cause actual results to differ materially include global political, economic, business, competitive, market, regulatory and other factors and risks, such as: the impact of macroeconomic conditions and whether industry trends we have identified develop as anticipated, including the future impacts of the novel coronavirus disease (“COVID-19”) outbreak and measures taken in response thereto for which future developments are highly uncertain and difficult to predict; retaining existing partners and attracting new partners, concentration of our revenue in a small number of partners, and promotion and support of our products by our partners; cyber-attacks or other security breaches; disruptions in the operations of our and our outsourced partners' computer systems and data centers; the financial performance of our partners; the sufficiency of our allowance for credit losses and the accuracy of the assumptions or estimates used in preparing our financial statements, including those related to the CECL accounting guidance; higher borrowing costs and adverse financial market conditions impacting our funding and liquidity, and any reduction in our credit ratings; our ability to grow our deposits in the future; damage to our reputation; our ability to securitize our loan receivables, occurrence of an early amortization of our securitization facilities, loss of the right to service or subservice our securitized loan receivables, and lower payment rates on our securitized loan receivables; changes in market interest rates and the impact of any margin compression; effectiveness of our risk management processes and procedures, reliance on models which may be inaccurate or misinterpreted, our ability to manage our credit risk; our ability to offset increases in our costs in retailer share arrangements; competition in the consumer finance industry; our concentration in the U.S. consumer credit market; our ability to successfully develop and commercialize new or enhanced products and services; our ability to realize the value of acquisitions and strategic investments; reductions in interchange fees; fraudulent activity; failure of third-parties to provide various services that are important to our operations; international risks and compliance and regulatory risks and costs associated with international operations; alleged infringement of intellectual property rights of others and our ability to protect our intellectual property; litigation and regulatory actions; our ability to attract, retain and motivate key officers and employees; tax legislation initiatives or challenges to our tax positions and/or interpretations, and state sales tax rules and regulations; regulation, supervision, examination and enforcement of our business by governmental authorities, the impact of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) and other legislative and regulatory developments and the impact of the Consumer Financial Protection Bureau's (the “CFPB”) regulation of our business; impact of capital adequacy rules and liquidity requirements; restrictions that limit our ability to pay dividends and repurchase our common stock, and restrictions that limit the Bank’s ability to pay dividends to us; regulations relating to privacy, information security and data protection; use of third-party vendors and ongoing third-party business relationships; and failure to comply with anti-money laundering and anti-terrorism financing laws.

For the reasons described above, we caution you against relying on any forward-looking statements, which should also be read in conjunction with the other cautionary statements that are included elsewhere in this report and in our public filings, including under the heading “Risk Factors Relating to Our Business” and “Risk Factors Relating to Regulation” in our 2021 Form 10-K. You should not consider any list of such factors to be an exhaustive statement of all of the risks, uncertainties, or potentially inaccurate assumptions that could cause our current expectations or beliefs to change. Further, any forward-looking statement speaks only as of the date on which it is made, and we undertake no obligation to update or revise any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events, except as otherwise may be required by law.

PART I. FINANCIAL INFORMATION

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our condensed consolidated financial statements and related notes included elsewhere in this quarterly report and in our 2021 Form 10-K. The discussion below contains forward-looking statements that are based upon current expectations and are subject to uncertainty and changes in circumstances. Actual results may differ materially from these expectations. See “Cautionary Note Regarding Forward-Looking Statements.”

Introduction and Business Overview

____________________________________________________________________________________________

We are a premier consumer financial services company delivering one of the industry's most complete, digitally-enabled product suites. Our experience, expertise and scale encompass a broad spectrum of industries including digital, health and wellness, retail, telecommunications, home, auto, outdoor, pet and more. We have an established and diverse group of national and regional retailers, local merchants, manufacturers, buying groups, industry associations and healthcare service providers, which we refer to as our “partners.” For the three and nine months ended September 30, 2022, we financed $44.6 billion and $132.3 billion of purchase volume, respectively, and had 66.3 million and 68.5 million average active accounts, respectively, and at September 30, 2022, we had $86.0 billion of loan receivables.

We offer our credit products primarily through our wholly-owned subsidiary, the Bank. In addition, through the Bank, we offer, directly to retail, affinity relationships and commercial customers, a range of deposit products insured by the Federal Deposit Insurance Corporation (“FDIC”), including certificates of deposit, individual retirement accounts (“IRAs”), money market accounts, savings accounts and sweep and affinity deposits. We also take deposits at the Bank through third-party securities brokerage firms that offer our FDIC-insured deposit products to their customers. We have significantly expanded our online direct banking operations in recent years and our deposit base serves as a source of stable and diversified low cost funding for our credit activities. At September 30, 2022, we had $68.4 billion in deposits, which represented 82% of our total funding sources.

Our Sales Platforms

_________________________________________________________________

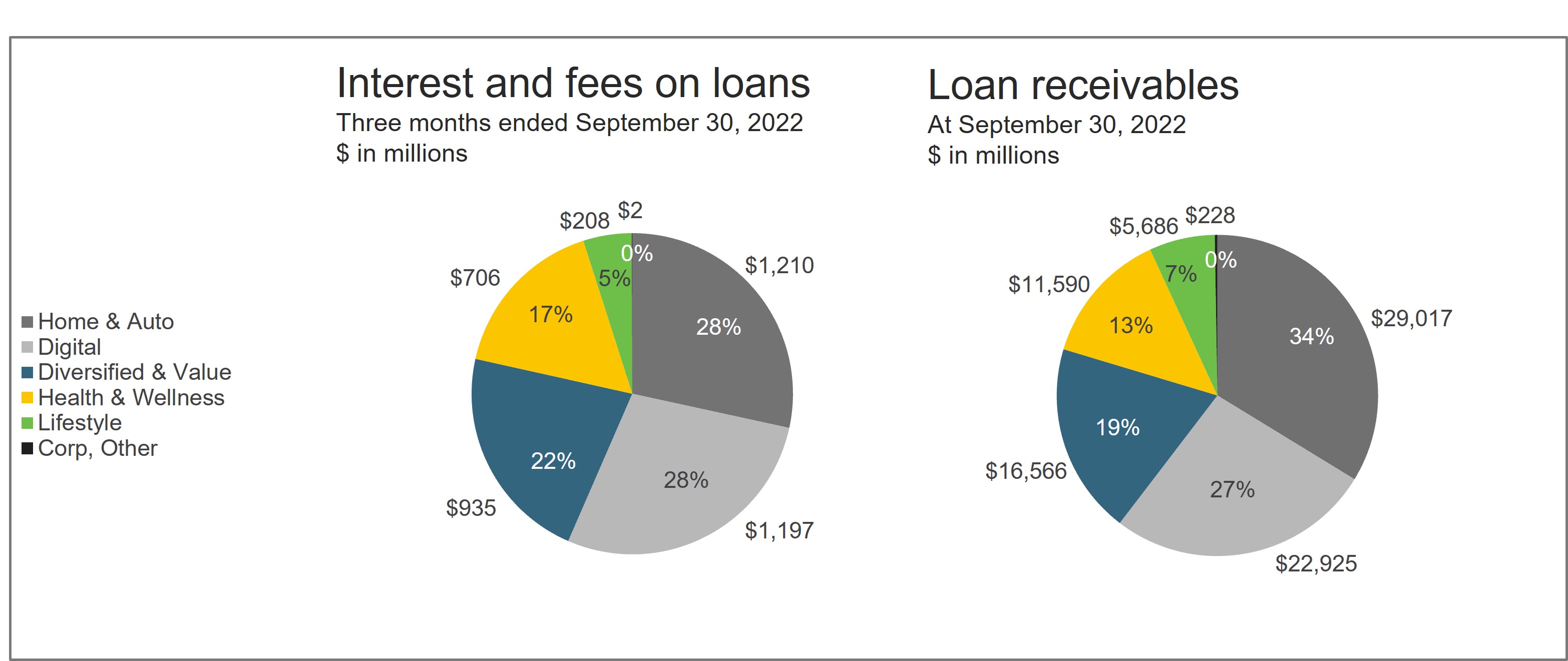

We conduct our operations through a single business segment. Profitability and expenses, including funding costs, credit losses and operating expenses, are managed for the business as a whole. Substantially all of our revenue activities are within the United States. We primarily manage our credit products through five sales platforms (Home & Auto, Digital, Diversified & Value, Health & Wellness and Lifestyle). Those platforms are organized by the types of partners we work with, and are measured on interest and fees on loans, loan receivables, active accounts and other sales metrics.

Home & Auto

Our Home & Auto sales platform provides comprehensive payments and financing solutions with integrated in-store and digital experiences through a broad network of partners and merchants providing home and automotive merchandise and services, as well as our Synchrony Car Care network and Synchrony HOME credit card offering. Our Home & Auto sales platform partners include a wide range of key retailers in the home improvement, furniture, bedding, appliance and electronics industry, such as Ashley HomeStores LTD, Lowe's, and Mattress Firm, as well as automotive merchandise and services, such as Chevron and Discount Tire. In addition, we also have program agreements with buying groups, manufacturers and industry associations, such as Nationwide Marketing Group and the Home Furnishings Association.

Digital

Our Digital sales platform provides comprehensive payments and financing solutions with integrated digital experiences through partners and merchants who primarily engage with their consumers through digital channels. Our Digital sales platform includes key partners delivering digital payment solutions, such as PayPal, including our Venmo program, online marketplaces, such as Amazon and eBay, and digital-first brands and merchants, such as Verizon, the Qurate brands, and Fanatics.

Diversified & Value

Our Diversified & Value sales platform provides comprehensive payments and financing solutions with integrated in-store and digital experiences through large retail partners who deliver everyday value to consumers shopping for daily needs or important life moments. Our Diversified & Value sales platform is comprised of five large retail partners: Belk, Fleet Farm, JCPenney, Sam's Club and TJX Companies, Inc.

Health & Wellness

Our Health & Wellness sales platform provides comprehensive healthcare payments and financing solutions, through a network of providers and health systems, for those seeking health and wellness care for themselves, their families and their pets, and includes key brands such as CareCredit and Pets Best, as well as partners such as Walgreens.

Lifestyle

Lifestyle provides comprehensive payments and financing solutions with integrated in-store and digital experiences through partners and merchants who offer merchandise in power sports, outdoor power equipment, and other industries such as sporting goods, apparel, jewelry and music. Our Lifestyle sales platform partners include a wide range of key retailers in the apparel, specialty retail, outdoor, music and luxury industry, such as

American Eagle, Dick's Sporting Goods, Guitar Center, Polaris and Pandora.

Corp, Other

Corp, Other includes activity and balances related to certain program agreements with retail partners and merchants that will not be renewed beyond their current expiry date and certain programs that were previously terminated, which are not managed within the five sales platforms discussed above, and for the nine months ended September 30, 2022 primarily includes activity associated with the Gap Inc. and BP portfolios, which were both sold in the second quarter of 2022. Corp, Other also includes amounts related to changes in the fair value of equity investments and realized gains or losses associated with the sale of investments.

Our Credit Products

____________________________________________________________________________________________

Through our sales platforms, we offer three principal types of credit products: credit cards, commercial credit products and consumer installment loans. We also offer a debt cancellation product.

The following table sets forth each credit product by type and indicates the percentage of our total loan receivables that are under standard terms only or pursuant to a promotional financing offer at September 30, 2022.

| | | | | | | | | | | | | | | | | | | | | | | |

| | | Promotional Offer | | |

| Credit Product | Standard Terms Only | | Deferred Interest | | Other Promotional | | Total |

| Credit cards | 57.7 | % | | 20.6 | % | | 16.2 | % | | 94.5 | % |

| Commercial credit products | 2.0 | | | — | | | — | | | 2.0 | |

| Consumer installment loans | — | | | 0.1 | | | 3.3 | | | 3.4 | |

| Other | 0.1 | | | — | | | — | | | 0.1 | |

| Total | 59.8 | % | | 20.7 | % | | 19.5 | % | | 100.0 | % |

Credit Cards

We offer the following principal types of credit cards:

•Private Label Credit Cards. Private label credit cards are partner-branded credit cards (e.g., Lowe’s or Amazon) or program-branded credit cards (e.g., Synchrony Car Care or CareCredit) that are used primarily for the purchase of goods and services from the partner or within the program network. In addition, in some cases, cardholders may be permitted to access their credit card accounts for cash advances. Credit under our private label credit cards typically is extended either on standard terms only or pursuant to a promotional financing offer.

•Dual Cards and General Purpose Co-Branded Cards. Our patented Dual Cards are credit cards that function as private label credit cards when used to purchase goods and services from our partners, and as general purpose credit cards when used to make purchases from other retailers wherever cards from those card networks are accepted or for cash advance transactions. We also offer general purpose co-branded credit cards that do not function as private label credit cards, as well as a Synchrony-branded general purpose credit card. Dual Cards and general purpose co-branded credit cards are offered across all of our sales platforms and credit is typically extended on standard terms only. We offer either Dual Cards or general purpose co-branded credit cards through approximately 20 of our large retail partners, of which the majority are Dual Cards, as well as our CareCredit Dual Card. Consumer Dual Cards and Co-Branded cards totaled 23% of our total loan receivables portfolio at September 30, 2022.

Commercial Credit Products

We offer private label cards and Dual Cards for commercial customers that are similar to our consumer offerings. We also offer a commercial pay-in-full accounts receivable product to a wide range of business customers.

Installment Loans

We originate installment loans to consumers (and a limited number of commercial customers) in the United States, primarily in the power products market (motorcycles, ATVs and lawn and garden), as well as through our various SetPay installment products (such as our SetPay Pay in 4 product for short-term loans). Installment loans are closed-end credit accounts where the customer pays down the outstanding balance in installments. Installment loans are generally assessed periodic finance charges using fixed interest rates.

Business Trends and Conditions

____________________________________________________________________________________________

We believe our business and results of operations will be impacted in the future by various trends and conditions. For a discussion of certain trends and conditions, see “Management's Discussion and Analysis of Financial Condition and Results of Operations—Business Trends and Conditions” in our 2021 Form 10-K. For a discussion of how certain trends and conditions impacted the three and nine months ended September 30, 2022, see “—Results of Operations.”

Seasonality

____________________________________________________________________________________________

We experience fluctuations in transaction volumes and the level of loan receivables as a result of higher seasonal consumer spending and payment patterns that typically result in an increase of loan receivables from August through a peak in late December, with reductions in loan receivables typically occurring over the first and second quarters of the following year as customers pay their balances down.

The seasonal impact to transaction volumes and the loan receivables balance typically results in fluctuations in our results of operations, delinquency metrics and the allowance for credit losses as a percentage of total loan receivables between quarterly periods.

In addition to the seasonal variance in loan receivables discussed above, we also typically experience a seasonal increase in delinquency rates and delinquent loan receivables balances during the third and fourth quarters of each year due to lower customer payment rates, resulting in higher net charge-off rates in the first and second quarters. Our delinquency rates and delinquent loan receivables balances typically decrease during the subsequent first and second quarters as customers begin to pay down their loan balances and return to current status, resulting in lower net charge-off rates in the third and fourth quarters. Because customers who were delinquent during the fourth quarter of a calendar year have a higher probability of returning to current status when compared to customers who are delinquent at the end of each of our interim reporting periods, we expect that a higher proportion of delinquent accounts outstanding at an interim period end will result in charge-offs, as compared to delinquent accounts outstanding at a year end. Consistent with this historical experience, we generally experience a higher allowance for credit losses as a percentage of total loan receivables at the end of an interim period, as compared to the end of a calendar year. In addition, despite improving credit metrics such as declining past due amounts, we may experience an increase in our allowance for credit losses at an interim period end compared to the prior year end, reflecting these same seasonal trends.

While the effects of the seasonal trends discussed above have remained evident during the nine months ended September 30, 2022, we also continue to experience elevated customer payment behavior, which include the effects of governmental stimulus actions, industry-wide forbearance measures and elevated consumer savings. While we have experienced some moderation in the three months ended September 30, 2022, customer payments as a percentage of beginning-of-period loan receivables remain significantly elevated compared to historical averages, and corresponding delinquency rates and net charge-off rates are below our historical average. During the three months ended September 30, 2022, we have experienced an increase in our delinquency rates that reflects both the seasonal trends discussed above and some moderation of customer payment rates.

Results of Operations

____________________________________________________________________________________________

Highlights for the Three and Nine Months Ended September 30, 2022

Below are highlights of our performance for the three and nine months ended September 30, 2022 compared to the three and nine months ended September 30, 2021, as applicable, except as otherwise noted.

•Net earnings decreased to $703 million from $1.1 billion and to $2.4 billion from $3.4 billion. The decreases in the three and nine months ended September 30, 2022 were primarily driven by increases in provision for credit losses due to reserve reductions in the prior year, partially offset by higher net interest income.

•Loan receivables increased 12.6% to $86.0 billion at September 30, 2022 compared to $76.4 billion at September 30, 2021, driven by strong purchase volume growth and some moderation of customer payment rates.

•Net interest income increased 7.4% to $3.9 billion and 10.7% to $11.5 billion for the three and nine months ended September 30, 2022, respectively. Interest and fees on loans increased 9.5% and 10.0% for the three and nine months ended September 30, 2022, respectively, primarily driven by growth in average loan receivables, partially offset by the impacts of portfolios sold in the second quarter of 2022. For the three and nine months ended September 30, 2022, interest expense increased due to higher benchmark rates and higher funding liabilities.

•Retailer share arrangements decreased 16.5% to $1.1 billion the three months ended September 30, 2022, primarily due to the impact of portfolios sold in the second quarter of 2022 and program performance. Retailer share arrangements remained relatively flat for the nine months ended September 30, 2022.

•Over-30 day loan delinquencies as a percentage of period-end loan receivables increased 86 basis points to 3.28% at September 30, 2022. The net charge-off rate increased 82 basis points to 3.00% and decreased 29 basis points to 2.82% for the three and nine months ended September 30, 2022, respectively.

•Provision for credit losses increased to $929 million from $25 million, and to $2.2 billion from $165 million for the three and nine months ended September 30, 2022, respectively. The increases for the three and nine months ended September 30, 2022, were primarily driven by reserve increases in the current year versus reserve reductions in the prior year periods. The increases in reserves for credit losses were $294 million and $414 million for the three and nine months ended September 30, 2022, respectively, and the reserve reductions for the corresponding prior year periods were $407 million and $1.6 billion, respectively. Our allowance coverage ratio (allowance for credit losses as a percent of period-end loan receivables) decreased to 10.58% at September 30, 2022, as compared to 11.28% at September 30, 2021.

•Other expense increased by $103 million, or 10.7%, and $345 million, or 12.1%, for the three and nine months ended September 30, 2022, respectively. The increase for the three months ended September 30, 2022 was primarily driven by increases in employee costs and other expense. The increase in the nine months ended September 30, 2022 was primarily driven by higher employee costs, other expense, information processing and marketing and business development.

•At September 30, 2022, deposits represented 82% of our total funding sources. Total deposits increased by 9.9% to $68.4 billion at September 30, 2022, compared to December 31, 2021.

•During the nine months ended September 30, 2022, we declared and paid cash dividends on our Series A 5.625% non-cumulative preferred stock of $42.18 per share, or $32 million.

•In April 2022, we announced that our Board approved an incremental share repurchase authorization of $2.8 billion through June 2023 and plans to increase our quarterly dividend by 5% to $0.23 per common share commencing in the third quarter of 2022. During the nine months ended September 30, 2022, we repurchased $2.6 billion of our outstanding common stock, and declared and paid cash dividends of $0.67 per share, or $331 million. At September 30, 2022 we have a total share repurchase authorization of $1.4 billion remaining. For more information, see “Capital—Dividend and Share Repurchases.”

2022 Partner Agreements

During the nine months ended September 30, 2022, we continued to expand and diversify our portfolio with the addition or renewal of more than 55 partners, which included the following:

•In our Home & Auto sales platform, we announced our new partnerships with Bassett, Floor & Decor and Furnitureland South and extended our agreements with Cardi's, Generac Power Systems, Home Zone, Ivan Smith Furniture, Mathis Brothers, Mattress Warehouse, Metro Mattress, Mitsubishi Electric Trane HVAC, NAPA AutoCare, New South Window Solutions, Regency Furniture Showrooms, Sleep Number and Sit 'N Sleep.

•In our Digital sales platform, we extended our program agreement with Shop HQ.

•In our Diversified & Value sales platform, we extended our program agreement with Fleet Farm.

•In our Health & Wellness sales platform, we expanded our network through our new partnerships with Buffalo Veterinary Group, Mission Veterinary Partners, Rarebreed Veterinary Partners, Service Corporation International, Smile Design Dentistry and Suveto and extended our agreements with Encore Vet Group, Interdent, Lucid and Sono Bello.

◦We expanded our partnership with AdventHealth to offer CareCredit as the primary patient financing solution across nationwide footprint.

◦We announced our integration with Sycle, to deliver a comprehensive financing solution suite.

•In our Lifestyle sales platform, we announced our new partnership with American Trailer World and extended our program agreements with Guitar Center, Janome, Kevin Jewelers, Kymco, Reeds, Sweetwater, Suzuki and Suzuki Marine.

•We launched our SetPay Pay in 4 buy now, pay later solution on the Clover point-of-sale and business management platform from Fiserv.

•We completed the sales of a total of $3.8 billion of loan receivables associated with our program agreements with Gap Inc. and BP during the second quarter of 2022, and recognized a gain on sale of $120 million included within other income in our condensed consolidated statement of earnings.

Summary Earnings

The following table sets forth our results of operations for the periods indicated.

| | | | | | | | | | | | | | | | | | | | | | | |

| Three months ended September 30, | | Nine months ended September 30, |

| ($ in millions) | 2022 | | 2021 | | 2022 | | 2021 |

| Interest income | $ | 4,342 | | | $ | 3,898 | | | $ | 12,438 | | | $ | 11,218 | |

| Interest expense | 414 | | | 240 | | | 919 | | | 809 | |

| Net interest income | 3,928 | | | 3,658 | | | 11,519 | | | 10,409 | |

| Retailer share arrangements | (1,057) | | | (1,266) | | | (3,288) | | | (3,261) | |

| | | | | | | |

| Provision for credit losses | 929 | | | 25 | | | 2,174 | | | 165 | |

| Net interest income, after retailer share arrangements and provision for credit losses | 1,942 | | | 2,367 | | | 6,057 | | | 6,983 | |

| Other income | 44 | | | 94 | | | 350 | | | 314 | |

| Other expense | 1,064 | | | 961 | | | 3,186 | | | 2,841 | |

| Earnings before provision for income taxes | 922 | | | 1,500 | | | 3,221 | | | 4,456 | |

| Provision for income taxes | 219 | | | 359 | | | 782 | | | 1,048 | |

| Net earnings | $ | 703 | | | $ | 1,141 | | | $ | 2,439 | | | $ | 3,408 | |

| Net earnings available to common stockholders | $ | 692 | | | $ | 1,130 | | | $ | 2,407 | | | $ | 3,376 | |

Other Financial and Statistical Data

The following table sets forth certain other financial and statistical data for the periods indicated.

| | | | | | | | | | | | | | | | | | | | | | | |

| At and for the | | At and for the |

| Three months ended September 30, | | Nine months ended September 30, |

| ($ in millions) | 2022 | | 2021 | | 2022 | | 2021 |

| Financial Position Data (Average): | | | | | | | |

| Loan receivables, including held for sale | $ | 84,038 | | | $ | 78,714 | | | $ | 83,404 | | | $ | 77,965 | |

| Total assets | $ | 98,694 | | | $ | 91,948 | | | $ | 96,786 | | | $ | 93,915 | |

| Deposits | $ | 67,158 | | | $ | 59,633 | | | $ | 64,751 | | | $ | 61,258 | |

| Borrowings | $ | 13,360 | | | $ | 13,522 | | | $ | 13,645 | | | $ | 14,528 | |

| Total equity | $ | 13,238 | | | $ | 14,117 | | | $ | 13,475 | | | $ | 13,619 | |

| Selected Performance Metrics: | | | | | | | |

Purchase volume(1)(2) | $ | 44,557 | | | $ | 41,912 | | | $ | 132,264 | | | $ | 118,782 | |

| Home & Auto | $ | 12,273 | | | $ | 11,069 | | | $ | 35,428 | | | $ | 31,929 | |

| Digital | $ | 12,941 | | | $ | 10,980 | | | $ | 36,600 | | | $ | 31,250 | |

| Diversified & Value | $ | 14,454 | | | $ | 12,006 | | | $ | 40,400 | | | $ | 32,844 | |

| Health & Wellness | $ | 3,514 | | | $ | 3,024 | | | $ | 10,064 | | | $ | 8,660 | |

| Lifestyle | $ | 1,374 | | | $ | 1,298 | | | $ | 4,000 | | | $ | 3,857 | |

| Corp, Other | $ | 1 | | | $ | 3,535 | | | $ | 5,772 | | | $ | 10,242 | |

Average active accounts (in thousands)(2)(3) | 66,266 | | | 67,189 | | | 68,517 | | | 66,500 | |

Net interest margin(4) | 15.52 | % | | 15.45 | % | | 15.64 | % | | 14.40 | % |

| Net charge-offs | $ | 635 | | | $ | 432 | | | $ | 1,760 | | | $ | 1,815 | |

| Net charge-offs as a % of average loan receivables, including held for sale | 3.00 | % | | 2.18 | % | | 2.82 | % | | 3.11 | % |

Allowance coverage ratio(5) | 10.58 | % | | 11.28 | % | | 10.58 | % | | 11.28 | % |

Return on assets(6) | 2.8 | % | | 4.9 | % | | 3.4 | % | | 4.9 | % |

Return on equity(7) | 21.1 | % | | 32.1 | % | | 24.2 | % | | 33.5 | % |

Equity to assets(8) | 13.41 | % | | 15.35 | % | | 13.92 | % | | 14.50 | % |

| Other expense as a % of average loan receivables, including held for sale | 5.02 | % | | 4.84 | % | | 5.11 | % | | 4.87 | % |

Efficiency ratio(9) | 36.5 | % | | 38.7 | % | | 37.1 | % | | 38.1 | % |

| Effective income tax rate | 23.8 | % | | 23.9 | % | | 24.3 | % | | 23.5 | % |

| Selected Period-End Data: | | | | | | | |

| Loan receivables | $ | 86,012 | | | $ | 76,388 | | | $ | 86,012 | | | $ | 76,388 | |

| Allowance for credit losses | $ | 9,102 | | | $ | 8,616 | | | $ | 9,102 | | | $ | 8,616 | |

30+ days past due as a % of period-end loan receivables(10) | 3.28 | % | | 2.42 | % | | 3.28 | % | | 2.42 | % |

90+ days past due as a % of period-end loan receivables(10) | 1.43 | % | | 1.05 | % | | 1.43 | % | | 1.05 | % |

Total active accounts (in thousands)(2)(3) | 66,503 | | | 67,245 | | | 66,503 | | | 67,245 | |

______________________(1)Purchase volume, or net credit sales, represents the aggregate amount of charges incurred on credit cards or other credit product accounts less returns during the period.

(2)Includes activity and accounts associated with loan receivables held for sale.

(3)Active accounts represent credit card or installment loan accounts on which there has been a purchase, payment or outstanding balance in the current month.

(4)Net interest margin represents net interest income divided by average interest-earning assets.

(5)Allowance coverage ratio represents allowance for credit losses divided by total period-end loan receivables.

(6)Return on assets represents net earnings as a percentage of average total assets.

(7)Return on equity represents net earnings as a percentage of average total equity.

(8)Equity to assets represents average total equity as a percentage of average total assets.

(9)Efficiency ratio represents (i) other expense, divided by (ii) sum of net interest income, plus other income, less retailer share arrangements.

(10)Based on customer statement-end balances extrapolated to the respective period-end date.

Average Balance Sheet

The following tables set forth information for the periods indicated regarding average balance sheet data, which are used in the discussion of interest income, interest expense and net interest income that follows.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 2022 | | 2021 | | |

| Three months ended September 30 ($ in millions) | Average

Balance | | Interest

Income /

Expense | | Average Yield / Rate(1) | | Average

Balance | | Interest

Income/

Expense | | Average Yield / Rate(1) | | |

| Assets | | | | | | | | | | | | | |

| Interest-earning assets: | | | | | | | | | | | | | |

Interest-earning cash and equivalents(2) | $ | 11,506 | | | $ | 65 | | | 2.24 | % | | $ | 9,559 | | | $ | 3 | | | 0.12 | % | | |

| Securities available for sale | 4,861 | | | 19 | | | 1.55 | % | | 5,638 | | | 8 | | | 0.56 | % | | |

Loan receivables, including held for sale(3): | | | | | | | | | | | | | |

| Credit cards | 79,354 | | | 4,153 | | | 20.76 | % | | 74,686 | | | 3,793 | | | 20.15 | % | | |

| Consumer installment loans | 2,884 | | | 74 | | | 10.18 | % | | 2,555 | | | 64 | | | 9.94 | % | | |

| Commercial credit products | 1,720 | | | 30 | | | 6.92 | % | | 1,407 | | | 29 | | | 8.18 | % | | |

| Other | 80 | | | 1 | | | 4.96 | % | | 66 | | | 1 | | | NM | | |

| Total loan receivables, including held for sale | 84,038 | | | 4,258 | | | 20.10 | % | | 78,714 | | | 3,887 | | | 19.59 | % | | |

| Total interest-earning assets | 100,405 | | | 4,342 | | | 17.16 | % | | 93,911 | | | 3,898 | | | 16.47 | % | | |

| Non-interest-earning assets: | | | | | | | | | | | | | |

| Cash and due from banks | 1,580 | | | | | | | 1,588 | | | | | | | |

| Allowance for credit losses | (8,878) | | | | | | | (8,956) | | | | | | | |

| Other assets | 5,587 | | | | | | | 5,405 | | | | | | | |

| Total non-interest-earning assets | (1,711) | | | | | | | (1,963) | | | | | | | |

| Total assets | $ | 98,694 | | | | | | | $ | 91,948 | | | | | | | |

| Liabilities | | | | | | | | | | | | | |

| Interest-bearing liabilities: | | | | | | | | | | | | | |

| Interest-bearing deposit accounts | $ | 66,787 | | | $ | 280 | | | 1.66 | % | | $ | 59,275 | | | $ | 131 | | | 0.88 | % | | |

| Borrowings of consolidated securitization entities | 6,258 | | | 54 | | | 3.42 | % | | 7,051 | | | 41 | | | 2.31 | % | | |

| | | | | | | | | | | | | |

| Senior unsecured notes | 7,102 | | | 80 | | | 4.47 | % | | 6,471 | | | 68 | | | 4.17 | % | | |

| | | | | | | | | | | | | |

| Total interest-bearing liabilities | 80,147 | | | 414 | | | 2.05 | % | | 72,797 | | | 240 | | | 1.31 | % | | |

| Non-interest-bearing liabilities: | | | | | | | | | | | | | |

| Non-interest-bearing deposit accounts | 371 | | | | | | | 358 | | | | | | | |

| Other liabilities | 4,938 | | | | | | | 4,676 | | | | | | | |

| Total non-interest-bearing liabilities | 5,309 | | | | | | | 5,034 | | | | | | | |

| Total liabilities | 85,456 | | | | | | | 77,831 | | | | | | | |

| Equity | | | | | | | | | | | | | |

| Total equity | 13,238 | | | | | | | 14,117 | | | | | | | |

| Total liabilities and equity | $ | 98,694 | | | | | | | $ | 91,948 | | | | | | | |

Interest rate spread(4) | | | | | 15.11 | % | | | | | | 15.16 | % | | |

| Net interest income | | | $ | 3,928 | | | | | | | $ | 3,658 | | | | | |

Net interest margin(5) | | | | | 15.52 | % | | | | | | 15.45 | % | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 2022 | | 2021 | | |

| Nine months ended September 30 ($ in millions) | Average

Balance | | Interest

Income /

Expense | | Average Yield / Rate(1) | | Average

Balance | | Interest

Income/

Expense | | Average Yield / Rate(1) | | |

| Assets | | | | | | | | | | | | | |

| Interest-earning assets: | | | | | | | | | | | | | |

Interest-earning cash and equivalents(2) | $ | 9,920 | | | $ | 90 | | | 1.21 | % | | $ | 12,567 | | | $ | 11 | | | 0.12 | % | | |

| Securities available for sale | 5,143 | | | 43 | | | 1.12 | % | | 6,128 | | | 21 | | | 0.46 | % | | |

Loan receivables, including held for sale(3): | | | | | | | | | | | | | |

| Credit cards | 78,946 | | | 12,009 | | | 20.34 | % | | 74,179 | | | 10,934 | | | 19.71 | % | | |

| Consumer installment loans | 2,781 | | | 209 | | | 10.05 | % | | 2,398 | | | 176 | | | 9.81 | % | | |

| Commercial credit products | 1,604 | | | 83 | | | 6.92 | % | | 1,334 | | | 73 | | | 7.32 | % | | |

| Other | 73 | | | 4 | | | 7.33 | % | | 54 | | | 3 | | | 7.43 | % | | |

| Total loan receivables, including held for sale | 83,404 | | | 12,305 | | | 19.73 | % | | 77,965 | | | 11,186 | | | 19.18 | % | | |

| Total interest-earning assets | 98,467 | | | 12,438 | | | 16.89 | % | | 96,660 | | | 11,218 | | | 15.52 | % | | |

| Non-interest-earning assets: | | | | | | | | | | | | | |

| Cash and due from banks | 1,607 | | | | | | | 1,594 | | | | | | | |

| Allowance for credit losses | (8,735) | | | | | | | (9,656) | | | | | | | |

| Other assets | 5,447 | | | | | | | 5,317 | | | | | | | |

| Total non-interest-earning assets | (1,681) | | | | | | | (2,745) | | | | | | | |

| Total assets | $ | 96,786 | | | | | | | $ | 93,915 | | | | | | | |

| Liabilities | | | | | | | | | | | | | |

| Interest-bearing liabilities: | | | | | | | | | | | | | |

| Interest-bearing deposit accounts | $ | 64,371 | | | $ | 567 | | | 1.18 | % | | $ | 60,907 | | | $ | 447 | | | 0.98 | % | | |

| Borrowings of consolidated securitization entities | 6,547 | | | 127 | | | 2.59 | % | | 7,296 | | | 136 | | | 2.49 | % | | |

| | | | | | | | | | | | | |

| Senior unsecured notes | 7,098 | | | 225 | | | 4.24 | % | | 7,232 | | | 226 | | | 4.18 | % | | |

| | | | | | | | | | | | | |

| Total interest-bearing liabilities | 78,016 | | | 919 | | | 1.57 | % | | 75,435 | | | 809 | | | 1.43 | % | | |

| Non-interest-bearing liabilities: | | | | | | | | | | | | | |

| Non-interest-bearing deposit accounts | 380 | | | | | | | 351 | | | | | | | |

| Other liabilities | 4,915 | | | | | | | 4,510 | | | | | | | |

| Total non-interest-bearing liabilities | 5,295 | | | | | | | 4,861 | | | | | | | |

| Total liabilities | 83,311 | | | | | | | 80,296 | | | | | | | |

| Equity | | | | | | | | | | | | | |

| Total equity | 13,475 | | | | | | | 13,619 | | | | | | | |

| Total liabilities and equity | $ | 96,786 | | | | | | | $ | 93,915 | | | | | | | |

Interest rate spread(4) | | | | | 15.32 | % | | | | | | 14.09 | % | | |

| Net interest income | | | $ | 11,519 | | | | | | | $ | 10,409 | | | | | |

Net interest margin(5) | | | | | 15.64 | % | | | | | | 14.40 | % | | |

____________________(1)Average yields/rates are based on total interest income/expense over average balances.

(2)Includes average restricted cash balances of $688 million and $745 million for the three months ended September 30, 2022 and 2021, respectively, and $647 million and $570 million for the nine months ended September 30, 2022 and 2021, respectively.

(3)Interest income on loan receivables includes fees on loans of $676 million and $610 million for the three months ended September 30, 2022 and 2021, respectively, and $2.0 billion and $1.6 billion for the nine months ended September 30, 2022 and 2021, respectively.

(4)Interest rate spread represents the difference between the yield on total interest-earning assets and the rate on total interest-bearing liabilities.

(5)Net interest margin represents net interest income divided by average total interest-earning assets.

For a summary description of the composition of our key line items included in our Statements of Earnings, see Management's Discussion and Analysis of Financial Condition and Results of Operations in our 2021 Form 10-K.

Interest Income

Interest income increased by $444 million, or 11.4%, and $1.2 billion, or 10.9%, for the three and nine months ended September 30, 2022, respectively, primarily driven by increases in interest and fees on loans of 9.5% and 10.0%, respectively. The increases in interest and fees on loans were primarily driven by growth in average loan receivables, partially offset by the impacts of portfolios sold in the second quarter of 2022. Excluding the impact of the portfolio sales, interest and fees on loans increased 17.5% and 13.6% for the three and nine months ended September 30, 2022, respectively.

Average interest-earning assets

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three months ended September 30 ($ in millions) | 2022 | | % | | 2021 | | % | | | | |

| Loan receivables, including held for sale | $ | 84,038 | | | 83.7 | % | | $ | 78,714 | | | 83.8 | % | | | | |

| Liquidity portfolio and other | 16,367 | | | 16.3 | % | | 15,197 | | | 16.2 | % | | | | |

| Total average interest-earning assets | $ | 100,405 | | | 100.0 | % | | $ | 93,911 | | | 100.0 | % | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Nine months ended September 30 ($ in millions) | 2022 | | % | | 2021 | | % |

| Loan receivables, including held for sale | $ | 83,404 | | | 84.7 | % | | $ | 77,965 | | | 80.7 | % |

| Liquidity portfolio and other | 15,063 | | | 15.3 | % | | 18,695 | | | 19.3 | % |

| Total average interest-earning assets | $ | 98,467 | | | 100.0 | % | | $ | 96,660 | | | 100.0 | % |

Average loan receivables, including held for sale, increased 6.8% and 7.0% for the three and nine months ended September 30, 2022, respectively, primarily driven by growth in purchase volume, partially offset by the impacts from portfolios sold in the second quarter of 2022. Purchase volume increased 6.3% and 11.4% for the three and nine months ended September 30, 2022, respectively, and excluding the impact of portfolios sold during the second quarter, purchase volume increased by 16.1% and 16.4%, respectively.

Yield on average interest-earning assets

The yield on average interest-earning assets increased for the three and nine months ended September 30, 2022. The increase in the three months ended September 30, 2022 was primarily due to an increase in the yield on average loan receivables. The increase for the nine months ended September 30, 2022 was primarily due to an increase in the percentage of interest-earning assets attributable to loan receivables as well as an increase in the yield on average loan receivables. The increase in loan receivable yield was 51 basis points to 20.10% and 55 basis points to 19.73% for the three and nine months ended September 30, 2022, respectively.

Interest Expense

Interest expense increased by $174 million, or 72.5%, and $110 million, or 13.6%, for the three and nine months ended September 30, 2022, respectively, primarily attributed to benchmark interest rates and higher funding liabilities. Our cost of funds increased to 2.05% and 1.57% for the three and nine months ended September 30, 2022, respectively, compared to 1.31% and 1.43% for the three and nine months ended September 30, 2021, respectively.

Average interest-bearing liabilities

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three months ended September 30 ($ in millions) | 2022 | | % | | 2021 | | % | | | | |

| Interest-bearing deposit accounts | $ | 66,787 | | | 83.3 | % | | $ | 59,275 | | | 81.4 | % | | | | |

| Borrowings of consolidated securitization entities | 6,258 | | | 7.8 | % | | 7,051 | | | 9.7 | % | | | | |

| Senior unsecured notes | 7,102 | | | 8.9 | % | | 6,471 | | | 8.9 | % | | | | |

| | | | | | | | | | | |

| Total average interest-bearing liabilities | $ | 80,147 | | | 100.0 | % | | $ | 72,797 | | | 100.0 | % | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Nine months ended September 30 ($ in millions) | 2022 | | % | | 2021 | | % |

| Interest-bearing deposit accounts | $ | 64,371 | | | 82.5 | % | | $ | 60,907 | | | 80.7 | % |

| Borrowings of consolidated securitization entities | 6,547 | | | 8.4 | % | | 7,296 | | | 9.7 | % |

| Senior unsecured notes | 7,098 | | | 9.1 | % | | 7,232 | | | 9.6 | % |

| | | | | | | |

| Total average interest-bearing liabilities | $ | 78,016 | | | 100.0 | % | | $ | 75,435 | | | 100.0 | % |

Net Interest Income

Net interest income increased by $270 million, or 7.4%, and $1.1 billion, or 10.7%, for the three and nine months ended September 30, 2022, respectively, resulting from the changes in interest income and interest expense discussed above.

Retailer Share Arrangements

Retailer share arrangements decreased by $209 million, or 16.5%, for the three months ended September 30, 2022, primarily due to the impact of portfolios sold in the second quarter of 2022 and program performance. Retailer share arrangements remained relatively flat for the nine months ended September 30, 2022.

Provision for Credit Losses

Provision for credit losses increased to $929 million from $25 million, and to $2.2 billion from $165 million, for the three and nine months ended September 30, 2022, respectively. The increases for the three and nine months ended September 30, 2022 were primarily driven by reserve increases in the current year versus reserve reductions in the prior year periods. The increases in reserves for credit losses were $294 million and $414 million for the three and nine months ended September 30, 2022, respectively, and the reserve reductions for the corresponding prior year periods were $407 million and $1.6 billion, respectively.

Other Income

| | | | | | | | | | | | | | | | | | | | | | | |

| Three months ended September 30, | | Nine months ended September 30, |

| ($ in millions) | 2022 | | 2021 | | 2022 | | 2021 |

| Interchange revenue | $ | 238 | | | $ | 232 | | | $ | 731 | | | $ | 626 | |

| Debt cancellation fees | 103 | | | 70 | | | 285 | | | 205 | |

| Loyalty programs | (326) | | | (256) | | | (906) | | | (682) | |

| Other | 29 | | | 48 | | | 240 | | | 165 | |

| Total other income | $ | 44 | | | $ | 94 | | | $ | 350 | | | $ | 314 | |

Other income decreased by $50 million, or 53.2%, and increased $36 million, or 11.5%, for the three and nine months ended September 30, 2022, respectively. The decrease for the three months ended September 30, 2022 was primarily driven by higher loyalty program costs associated with purchase volume growth. The increase for the nine months ended September 30, 2022 was primarily driven by the recognition of the gain on sale of $120 million from the portfolio sales in the second quarter of 2022, as well as higher interchange revenue and debt cancellation fees, partially offset by higher loyalty program costs associated with purchase volume growth.

Other Expense

| | | | | | | | | | | | | | | | | | | | | | | |

| Three months ended September 30, | | Nine months ended September 30, |

| ($ in millions) | 2022 | | 2021 | | 2022 | | 2021 |

| Employee costs | $ | 416 | | | $ | 369 | | | $ | 1,222 | | | $ | 1,092 | |

| Professional fees | 204 | | | 196 | | | 599 | | | 575 | |

| Marketing and business development | 115 | | | 110 | | | 366 | | | 319 | |

| Information processing | 150 | | | 139 | | | 458 | | | 407 | |